Highlights

- People prosper most from free-market capitalism; we need more in America (and Texas).

- Americans are suffering from big-government policies out of D.C.

- This brief highlights more than just the headlines you usually get.

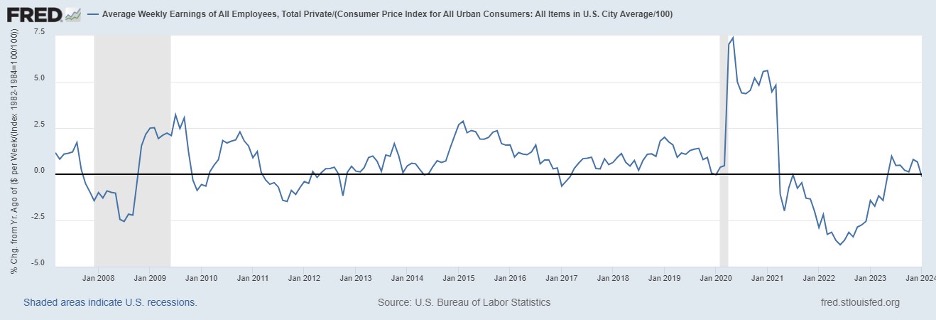

Figure 1: Real Average Weekly Earnings Remain Down 4.4% Since January 2021

Source: Fed FRED

Labor Market

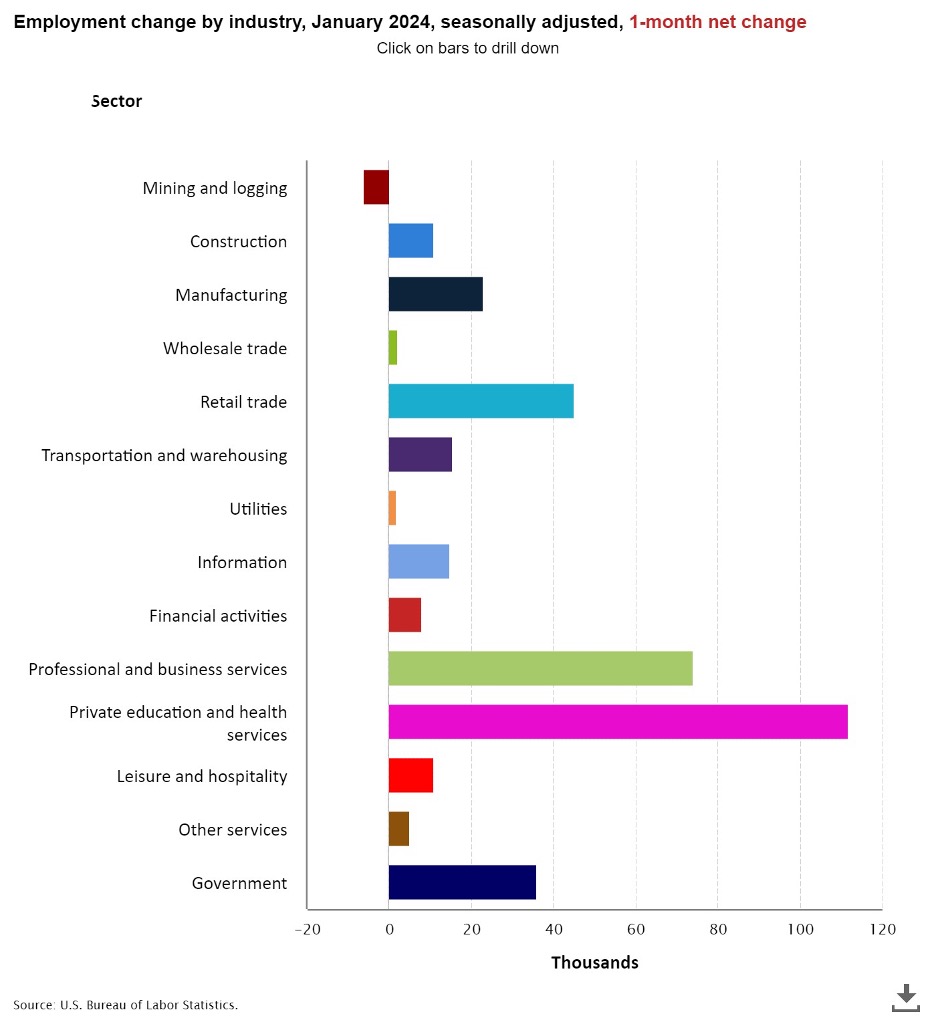

The Bureau of Labor Statistics recently released its U.S. jobs report for January 2024, which was another mixed report with some strengths but many weaknesses.

The establishment survey is the most reported.

- There were +353,000 net nonfarm jobs added in January to 157.7 million employees, which has increased by +2.9 million over the last year and +5.4 million since February 2020 before the COVID lockdowns.

- However, there continue to be large revisions for previous months as the data used for seasonal adjustments are from the last few years when there was substantial volatility in the labor market.

- Last month, there were +99,000 jobs added in the private sector and +36,000 jobs added in the government sector.

Source: Fed FRED

The household survey is important but often not reported.

- Employment fell by -31,000 jobs in January to 161.2 million employed. There have been declines in net employment in three of the last four for a total increase of +2.5 million since February 2020, which is well below the jobs added in the establishment survey.

- The labor force declined by -175,000 last month to 167.3 million. The labor force has declined in nine of the last 22 months and is up +3.1 million since March 2022 or up 2.9 million since February 2020.

- The unemployed declined by -144,000 last month, bringing the official U3 unemployment rate to 3.7%, and the broader U6 underutilization rate is at 7.2%.

- Since February 2020, the prime-age (25-54 years old) employment-population ratio has been flat at 80.6%, the prime-age labor force participation rate was 0.3 percentage points higher at 83.3%, and the total labor-force participation rate was 0.8-percentage-points lower at 62.5% with millions of people out of the labor force holding the U3 rate artificially low.

Economic Growth

The U.S. Bureau of Economic Analysis recently released the initial estimate for economic output in the fourth quarter of 2023.

Table 1 provides data over time for real total gross domestic product (GDP), measured in chained 2012 dollars, and real private GDP, which excludes government consumption expenditures and gross investment.

Table 1: Economic Output, Growth, and Inflation

| Q4/Q4 2021 | Q4/Q4 2022 | Q4/Q4 2023 | Q1:2023 | Q2:2023 | Q3:2023 | Q4:2023 | |

| Real total GDP (end of period) | $21.8T | $22.0T | $22.7T | $22.1T | $22.2T | $22.5T | $22.7T |

| Annualized growth (avg for period) | +5.4% | +0.7% | +3.1% | +2.2% | +2.1% | +4.9% | +3.3% |

| Real private GDP (end of period) | $18.2T | $18.3T | $18.8T | $18.4T | $18.4T | $18.6 | $18.8 |

| Annualized growth (avg for period) | +6.6% | +0.6% | +2.9% | +1.7% | +1.8% | +4.7% | +3.3% |

| GDP implicit inflation (avg for period) | +6.2% | +6.4% | +2.6% | +3.9% | +1.7% | +3.3% | +1.5% |

Another key measure of economic activity is the real average of GDP and GDI, which accounts for domestic production and income, but it hasn’t been released for the fourth quarter yet. The previous figure for the third quarter was an increase of 3.2%. This measure has declined in three of the last seven quarters, increasing this value by only 1.7% since the fourth quarter of 2021 before the two consecutive quarters of declines in the first and second quarters of 2022.

Meanwhile, the federal budget deficit is growing faster because of overspending and declining tax collections from a weak economy (see Figure 4). The national debt has ballooned to $34.3 trillion, and net interest payments on the debt will soon be a top federal expenditure, rising to above $1 trillion recently. The Federal Reserve has monetized, or printed, much of the new debt to keep interest rates artificially lower than where the market would have them. The Fed will need to cut its balance sheet (total assets over time) more aggressively if it is to stop manipulating markets (see this for types of assets on its balance sheet) and persistently tame inflation.

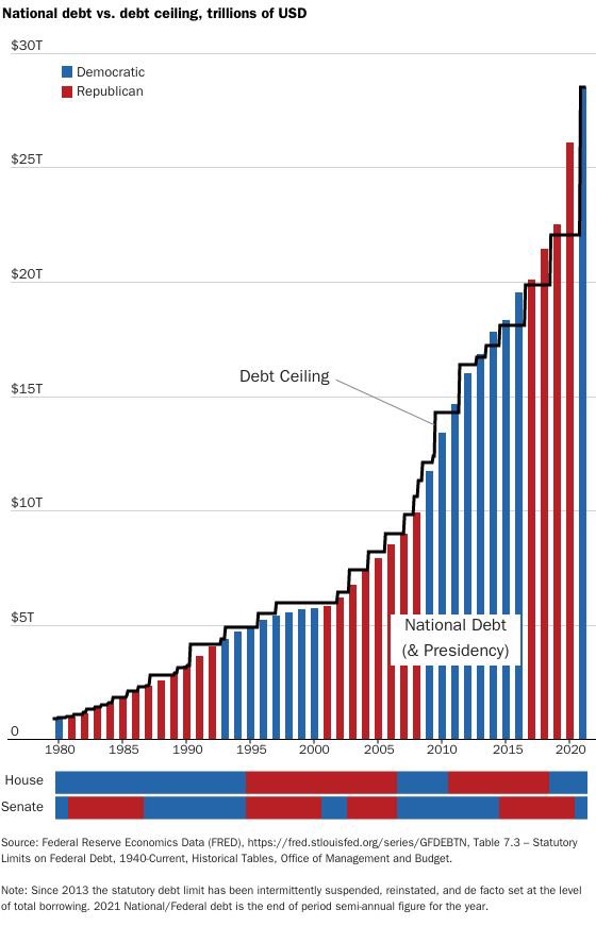

The current annual inflation rate of the consumer price index (CPI) has been cooling since a peak of +9.1% in June 2022 but remains elevated at 3.1% in January, which remains too high, as are other key measures of inflation. Just as inflation is always and everywhere a monetary phenomenon, deficits and high taxes are always and everywhere a spending problem. David Boaz at Cato Institute has noted how this problem is from both Republicans and Democrats (See Figure 3).

Figure 3: Rising Deficit-Spending Results from Democrats and Republicans

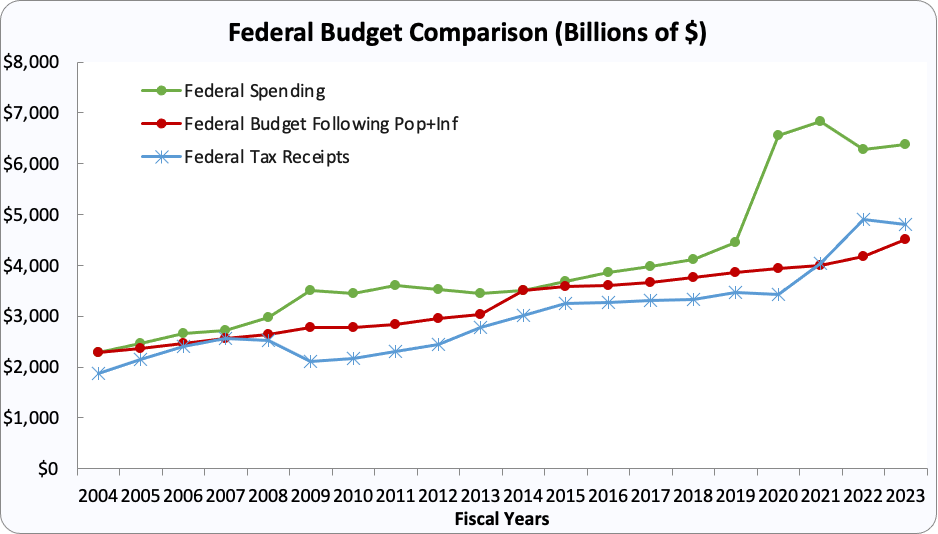

To control this fiscal crisis, which is contributing to a monetary crisis, the U.S. needs a fiscal rule like the Responsible American Budget (RAB) with a maximum spending limit based on the rate of population growth plus inflation. This was recently released as part of Americans for Tax Reform’s Sustainable Budget Project, highlighting this approach’s benefits at the federal, state, and local levels.

If Congress had followed this approach from 2004 to 2023, Figure 4 shows tax receipts, spending, and spending adjusted for only population growth plus chained-CPI inflation. Instead of an (updated) $20.2 trillion national debt increase, there could have been only a $700 billion debt increase for a $19.5 trillion swing in a positive direction that would have substantially reduced the cost of this debt to Americans. The Republican Study Committee recently noted the strength of this type of fiscal rule in its FY 2023 “Blueprint to Save America.” To top this off, the Federal Reserve should follow a monetary rule so that the costly discretion stops creating booms and busts.

Figure 4: Federal Budget Gap Shrinks If Spending Limited to Population Growth Plus Inflation

The Bottom Line

Bidenomics has been a complete failure and the policy approach must be redirected to pro-growth policies that shrink government rather than big-government, progressive policies. It’s time for a limited government with sound fiscal and monetary policy that provides more opportunities for people to work and have more paths out of poverty.

Recommendations:

- Set a pro-growth policy path with less spending, regulating, and taxing at all levels of government, which includes return-to-work policies.

- Reject new spending packages that America cannot afford nor needs; pass the RAB instead.

- Impose a strict monetary rule with the Fed having a much smaller balance sheet and a much higher federal funds rate targetuntil we End the Fed.

Texans for Fiscal Responsibility relies on the support of private donors across the Lone Star State in order to promote fiscal responsibility and pro-taxpayer government in Texas. Please consider supporting our efforts! Thank you!

Get The Fiscal Note, our free weekly roll-up on all the current events that could impact your wallet. Subscribe today!